What You Need to Know About the Serious Injury Threshold in New York in 2026

Image generated by Gemini

New York's motor vehicle litigation rules are shifting fast in 2026. Between surging claims, proposed legislative overhauls, and auto insurance premiums that keep climbing, drivers across the state are navigating a legal landscape that looks very different from even a year ago.

At the heart of it all is the state's "serious injury" threshold, the legal standard that determines whether you can sue for pain and suffering after a car crash. If you don't meet it, your recovery tops out at what no-fault insurance provides. And for a lot of people, that's not nearly enough.

The financial toll of traffic collisions has reached staggering levels. Fatal and serious crashes in New York recently resulted in an estimated $33.6 billion in economic costs. That number alone makes clear why lawmakers, insurers, and trial attorneys are all fighting over how the system should work going forward.

Surging personal injury filings have strained public budgets and private insurance markets alike. As a result, 2026 has brought efforts to redefine compensable harm and crack down on systemic fraud that's been driving up premiums for everyone.

How New York's No-Fault System Works

PIP Basics

New York operates under a strict no-fault insurance framework. The idea is simple: after a crash, your own insurer pays for initial medical treatment regardless of who caused it. The mandatory minimum PIP coverage required by law is $50,000 per person. That sounds like a decent safety net until you look at what things actually cost.

PIP covers 80% of lost earnings up to $2,000 per month for up to three years. It also allows up to $25 per day for one year to help cover daily necessities, such as household assistance. Those caps are rigid, and they often fall well short of what extended rehabilitation actually demands.

Consider the math. A basic ambulance ride in New York City runs between $1,000 and $1,700. An average ER visit? About $1,600. In a serious collision, you could blow through that entire $50,000 limit within days.

Local Impact

Urban density makes this problem worse. A lot worse. Localized data from 2024 shows that Brooklyn saw the highest volume of traffic collisions among the city's boroughs, with 22,781 crashes resulting in 9,990 injuries. That concentration puts enormous strain on regional medical infrastructure and insurance networks.

For drivers dealing with the financial fallout of a collision in that borough, knowing how to file for Brooklyn no-fault benefits properly is the critical first step before you even think about third-party liability.

The Serious Injury Threshold in 2026

Nine Categories of Compensable Harm

So what happens when your medical bills and lost wages blow past what PIP covers? You'll need to look at third-party litigation. But here's the catch: New York Insurance Law § 5102(d) defines nine specific categories you must meet to pursue non-economic damages like pain and suffering.

Here's what qualifies:

A fracture

Death or dismemberment

Significant disfigurement

Permanent significant limitation of the use of a body organ or member

Permanent loss of use of an organ, function, member, or system

Loss of a fetus

Significant limits to the use of a body function or system

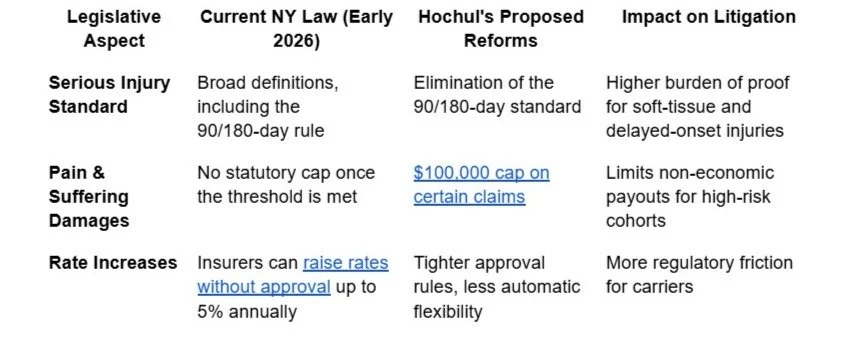

A medically determined injury that prevented you from doing normal daily activities for at least 90 of the 180 days right after the accident (the 90/180-day rule)

The 90/180-Day Rule Debate

This is where things get politically heated. Governor Hochul's 2026 reform package aims to narrow these criteria as part of a broader push to combat fraud and lower auto insurance premiums, which currently average nearly $4,000 annually. The administration argues that tighter medical standards will eliminate inefficiencies that burden the state insurance market.

The most contentious target? The 90/180-day rule. It's the most frequently litigated category under the threshold statute, and it's also the one that captures injuries that take time to show up. Critics of the reform, including the New York State Trial Lawyers Association and crash victims themselves, argue that eliminating this standard harms victims with delayed-onset trauma. Traumatic brain injuries (TBIs) and soft-tissue damage don't always announce themselves right away, which they say makes the time-based metric essential for fair recovery.

{kind=link}

Third-Party Liability and Recovery

How Comparative Negligence Works

New York subscribes to a pure comparative negligence system, which means even if you're partially at fault for an accident, you're not automatically shut out of financial recovery. Instead, the court figures out your total damages and reduces the award by your percentage of fault. If you're 30% responsible, you still collect 70% of the damages.

This framework has a big influence on settlement negotiations and trial strategy statewide. 2026 legislative proposals have attempted to modify payouts for people deemed "mostly" at fault for a collision. But those efforts face strong resistance from Albany lawmakers who prioritize victim compensation.

The Uninsured Motorist Problem

Pursuing third-party liability only works if the at-fault driver actually has insurance or assets worth going after. That's a real concern in New York, where an estimated 10.8 percent of drivers operate without insurance. Sound familiar? If you've been hit by one of them, you already know how vulnerable that leaves you.

When third-party litigation isn't viable because the at-fault driver is uninsured or underinsured, your recovery strategy has to shift. SUM coverage becomes critical in these situations, serving as your primary path to compensation. It's worth reviewing your Supplementary Uninsured/Underinsured Motorist policy limits now, because this is one of the most predictable risks on the road.

What's Next for New York Auto Litigation

The $50,000 PIP baseline keeps the lights on after a crash, but it rarely covers the full financial disruption of a serious collision. Getting real compensation means satisfying the state's evolving definition of a serious injury, and that requires thorough documentation of every medical treatment and functional limitation from day one.

Keep a close eye on the stalled 2026 state budget negotiations. The tug-of-war between state officials and trial lawyers will ultimately shape the regulatory environment. Those final decisions won't just affect premium costs; they'll determine how strict recovery limits are for years to come.