Best Out-of-State 529 Plans for New York Residents (Beyond NY 529 Direct)

Saving for college in New York usually starts with the state’s low-cost 529 Direct Plan. Built on Vanguard index funds, it lets you deduct up to $5,000 (single) or $10,000 (joint) on your state return—often worth $650 to $1,000 in cash each April. But that break applies only to your first dollars. Above the cap, fees and fund quality decide growth, and several out-of-state plans charge as little as 0.10 % a year—enough to outpace New York’s option over 18 years. This guide compares seven direct-sold 529s that give New York savers the best shot at higher net returns.

New York 529 tax perks and their ceiling

New York lets residents deduct up to $5,000 per year on a single return, or $10,000 on a joint return, when contributions go into the New York 529 Direct Plan. According to the New York State Department of Taxation and Finance, that break can trim roughly $650 to $1,000 from a typical combined state-and-city tax bill each year.

Because the deduction only applies to your first dollars, every contribution above the cap depends on fees, investment performance, and plan features. Many out-of-state plans charge lower expenses, so they can grow faster once the New York incentive runs out.

One caveat: if you move deducted money from the New York plan to another state’s 529, New York adds the prior deduction back to your taxable income for that year. The state removed this “recapture” rule for 529-to-Roth IRA rollovers in September 2024, keeping state law in step with the federal SECURE 2.0 change.

The rule applies only to dollars that claimed the deduction. Contribute directly to an out-of-state 529 and you avoid any future claw-back. That split-plan strategy—max the first $10,000 at home, then send overflow to the lowest-fee national leader—guides the rankings that follow.

New rules reshaping 529 strategy

529-to-Roth IRA rollovers: a fresh escape hatch

Starting in 2024, the SECURE 2.0 Act lets you move up to $35,000 of unused 529 money into the beneficiary’s Roth IRA. The rollover is federal-tax free, counts toward the annual Roth limit, and the 529 must be at least 15 years old with each contribution on file for five years.

For families worried about over-saving, this change turns leftover tuition dollars into retirement seed money with no penalties or income-cap hurdles.

New York closed its own gap on September 5, 2024, amending state tax law to treat 529-to-Roth rollovers as qualified withdrawals, according to CPAservices.com. Before that date, a rollover triggered recapture of any New York deduction. Now the state aligns with federal rules, so residents can move surplus balances without a tax claw-back.

The bottom line: whether you save in the New York 529 Direct Plan or an out-of-state option, any excess can now shift to a Roth IRA without a state-tax surprise.

Next up, we review the fee cuts and tech upgrades that have made several national plans cheaper and easier to use.

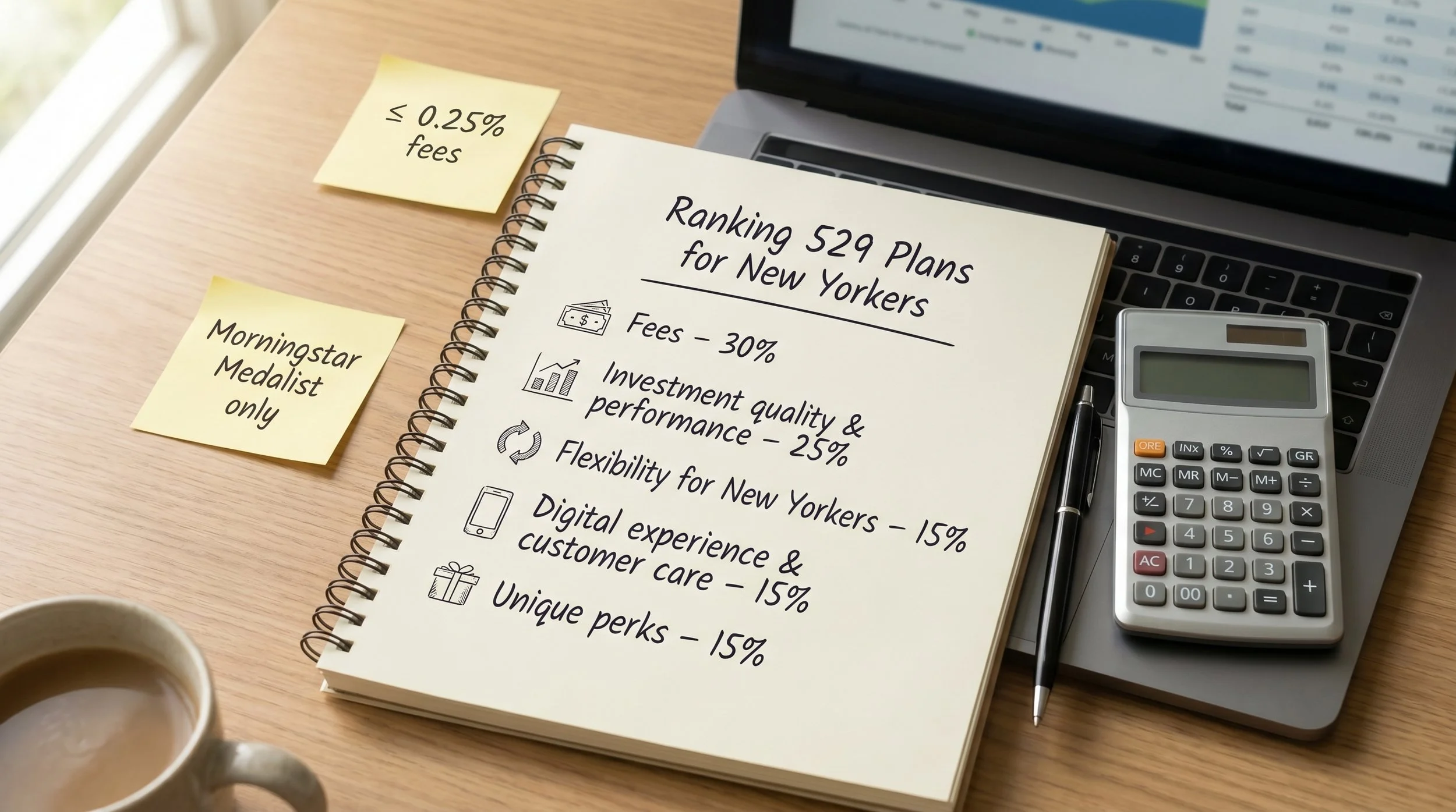

How we picked and ranked the contenders

We reviewed every direct-sold 529 plan in the country and scored each one using a five-factor system tailored to New York savers.

First comes cost: lower fees leave more money for tuition, so price carries the most weight. We then evaluated investment quality, flexibility, user experience, and any extra features that can tip the scales.

Weighting:

● Fees – 30 percent

● Investment quality and performance – 25 percent

● Flexibility for New Yorkers (easy funding, sensible minimums) – 15 percent

● Digital experience and customer care – 15 percent

● Unique perks (ESG funds, FDIC CDs, custom glide paths) – 15 percent

We applied strict guardrails. A plan had to charge 0.25 percent or less on its core age-based portfolio, accept out-of-state investors on equal terms, and hold a current Morningstar Medalist rating. Advisor-sold programs, load funds, or anything with hidden state surcharges went straight to the reject pile.

Finally, we gave bonus points for features that pair well with New York’s deduction, such as zero-dollar minimums or an easy rollover process. The outcome is a ranking that balances hard numbers with day-to-day usability for families who file in Albany.

Ready for the countdown? We start with number seven and work toward the top spot.

7. Virginia Invest529: a quiet overachiever worth a look

Virginia’s Invest529 rarely makes headlines, but it covers every practical need for New York savers.

Costs stay low. Most index portfolios sit near 0.13 percent all in, matching New York’s plan. The state agency continues to cut expenses as assets grow, so today’s price can fall further over time.

The investment menu feels familiar yet complete. Age-based tracks shift from growth to safety, while static options include U.S. equity, international, bonds, and an ESG-tilted balanced fund. BlackRock index funds provide broad diversification at a bargain price.

Ease matters, and Virginia scores well. The site is clean, works on mobile, and lets you set recurring deposits in minutes. Opening minimum: ten dollars, ideal for testing the waters after you max out your New York deduction.

Why is Virginia seventh? It lacks the ultra-low fees or special extras offered by higher-ranked plans. Still, if you want steady stewardship from a large 529 administrator and like an ESG sleeve without a surcharge, Invest529 is a reliable second account or a main home for dollars above Albany’s tax cap.

6. Nevada Vanguard 529: index efficiency for larger opening checks

Nevada’s direct 529 works much like holding a Vanguard brokerage account inside a tax shelter. Every portfolio relies on Vanguard index funds, so performance is transparent and fees predictable; most age-based tracks cost about 0.14 to 0.18 percent.

The trade-off appears on day one. Non-residents must deposit at least three thousand dollars to open an account. After that, additional contributions can be as low as fifty dollars.

Investment choice stays simple: choose an age-based glide path (conservative, moderate, or aggressive) or build from single funds such as Total Stock Market or Total Bond Market. There are no active sleeves, ESG detours, or bank stable-value funds. If you want market tracking at minimal cost, the Vanguard lineup delivers.

Platform integration strengthens the appeal. Because the plan lives on Vanguard’s website, you can see your 529 beside IRAs and taxable accounts, schedule automatic transfers from the same dashboard, and reach Vanguard phone reps if questions come up.

Why sixth place? The plan has competitive fees but fewer extras than the leaders, and its steep opening minimum can deter families easing into college savings. For households already deep in the Vanguard ecosystem and ready to write a larger first check, however, Nevada offers a clear, low-drag path to college funding.

5. Ohio CollegeAdvantage: versatility meets low costs

Ohio’s CollegeAdvantage ranks fifth for pairing one of the deepest investment menus in the 529 universe with fees in the low-teens basis-point range.

Start with choice. You can build a Vanguard index mix, tilt toward Dimensional Fund Advisors factor funds for a small-cap or value boost, or park near-college dollars in FDIC-insured CDs and a stable-value option that protects principal. Few plans bundle this breadth under one roof at a similar price.

Total expenses on the age-based index track run about 0.15 to 0.20 percent. The state tuition-trust authority reduces costs whenever assets cross a new milestone; a recent cut dropped the record-keeping fee below one-tenth of a percent.

User experience keeps pace. Opening an account takes about ten minutes online, the minimum is twenty-five dollars, and a gifting portal lets grandparents contribute with a few clicks. The dashboard even shows how much of your balance sits in each underlying fund, useful for tracking allocation.

For New Yorkers the strategy is simple: claim the home-state deduction on the first ten thousand dollars each year, then send overflow to Ohio if you want to blend growth assets for a toddler with principal-protected cash for a high-school junior in the same plan. No other program on this list matches that built-in flexibility.

Ohio finishes at number five because the remaining plans shave fees slightly lower or add standout perks. If menu depth and safety options top your list, the Buckeye plan is hard to beat.

4. Pennsylvania 529 Investment Plan: Vanguard strength with fee momentum

Pennsylvania’s direct-sold 529 looks like New York’s plan in many ways. It uses Vanguard index funds and stays easy to understand, but Harrisburg keeps trimming expenses whenever assets reach a new milestone.

The core age-based track costs about 0.20 percent today. The state treasury has negotiated several cuts in the past three years and publicly commits to lowering fees further as the program grows. You pay a low rate now and gain a path to even lower costs later.

The menu matches Vanguard’s greatest hits. Target Enrollment portfolios shift automatically as college nears, while static options cover total U.S. stock, international stock, bonds, and money market. The lineup is straightforward and fully diversified.

Why choose this plan over New York’s? First, governance diversification: Pennsylvania’s treasury runs the program and has a record of pressing fund providers on cost, giving your savings a second watchdog. Second, the plan requires only twenty-five dollars to open, so every dollar above New York’s deduction cap can move into a separate, low-fee account with almost no friction.

Pennsylvania ranks fourth because its price still sits a touch above the top three. Even so, the clear downward trend, Vanguard DNA, and strong state oversight make it an easy “set and forget” supplement for New York families seeking extra fee leverage without added complexity.

3. Massachusetts U.Fund: Fidelity index muscle, now Gold rated

Massachusetts once sat in the middle of the 529 pack. After cutting fees, trimming the fund menu, and securing a Morningstar Gold rating, U.Fund now feels custom-built for New Yorkers who already rely on Fidelity for retirement and brokerage accounts.

Costs come first. Age-based index portfolios run about 0.14 percent, matching New York and Illinois without locking you into Vanguard products. If you like Fidelity’s Total Market Index and want the same low-fee culture, this plan checks the box.

Investment choice stays simple. Select an age-based path that shifts from stocks to bonds, or place money in a few static index funds covering United States equity, international equity, and core bonds. No niche funds compete for attention, so decision fatigue stays low and glide-path discipline stays high.

Platform integration is the real draw. Open a U.Fund account and it appears next to your Fidelity balances under the same username and mobile app. Automatic transfers and college cost calculators live in the dashboard you already use, nudging you to stay on schedule.

Minimum to open? Zero dollars. Testing the plan after you exhaust New York’s deduction room is effortless. Because Massachusetts offers no resident tax break, out-of-staters pay the same fees and face no residency quirks.

Why third instead of higher? The lineup sticks to plain-vanilla index funds and lacks Utah’s custom controls or Illinois’s wider fund roster. If Fidelity integration and low fees top your wish list, though, U.Fund is a reliable, low-maintenance path to college savings.

2. Utah my529: customization at Vanguard-like prices

Utah’s my529 charges about 0.12 to 0.18 percent on its index age-based tracks while giving you a level of control few direct-sold plans match.

Utah my529 custom age-based portfolio interface.

Start with an off-the-shelf enrollment portfolio and you are set. Performance mirrors market indexes with minimal drag. Want deeper control? Select “Custom Age-Based” and craft your own glide path—for example, 70 percent stock through eighth grade before shifting to bonds—or add slices of small-cap value and real estate investment trusts. You can adjust the mix once each calendar quarter, balancing flexibility with discipline.

Access stays simple. The account has no opening minimum, and a gifting portal lets friends contribute through a personalized link. The site is clean and intuitive, a clear step up from New York’s interface.

Utah places second only because Illinois matches its fee tier while offering broader fund families and a new mobile app. If you enjoy tailoring asset allocation, my529 is the standout. For everyone else, it serves as a low-cost, high-quality companion to a core New York contribution strategy.

1. Illinois Bright Start: low-fee leader with steady upgrades

Bright Start ranks first because it pairs persistent fee cuts with broad investment choice. Most index portfolios cost about 0.13 percent, matching New York’s plan while adding fund families beyond Vanguard. In 2024 the Illinois treasurer negotiated another fee reduction and launched a mobile app that lets you open or fund an account in minutes.

Choice is extensive. More than forty portfolios draw from eleven fund managers, including Vanguard, DFA, and T. Rowe Price. You can stay with index funds or add selected active strategies without driving up cost. Age-based tracks offer several risk levels, and custom blends let experienced investors fine-tune allocation quickly.

Accessibility also stands out. The minimum to open is zero dollars, so Bright Start works well for the first dollar above New York’s deduction cap. You can set automatic transfers of any amount on any schedule, and there are no account or maintenance fees.

To test whether those transfers will cover a future tuition bill, Bright Start’s College savings plan estimator runs projections using a 6 percent annual return and 5 percent tuition inflation, then shows what share of costs your savings could fund.

Oversight adds confidence. The state treasurer’s office publishes each cost reduction and has earned Bright Start a Morningstar Gold rating for seven consecutive years, signaling a culture of continuous improvement.

Put together—low fees, a wide fund menu, and modern tools—Bright Start gives New York savers a strong chance to outpace the hometown plan on net returns.

Quick-glance comparison

Use this table to double-check fees and minimums before you open an account. Figures reflect plan disclosures through the fourth quarter of 2025, including the latest announced fee cuts.

*Morningstar Medalist ratings current as of the 2025 cycle.

Even a one-tenth-of-a-percentage-point fee gap on a one-hundred-thousand-dollar balance costs one hundred dollars every year. Compound that through senior year, and the low-cost leaders in the first three rows can cover a full semester of books by themselves.

FAQs for New York 529 savers

Do I lose the New York tax break if I use another state’s plan?

Yes. The deduction of up to five thousand dollars (single) or ten thousand dollars (joint) applies only to contributions made to the New York 529 Direct Plan.

Can I split my savings between two plans?

Yes. Many families claim the state deduction on the first ten thousand dollars each year, then send extra dollars to a low-fee out-of-state plan from our top seven list. The accounts run side by side, and the Internal Revenue Service and FAFSA treat them the same.

What happens if I roll New York money into another state’s 529 or a Roth IRA?

Moving funds to another state’s 529 triggers recapture of every New York deduction previously claimed on those contributions. A rollover to a Roth IRA is different: since September 5, 2024, New York treats a 529-to-Roth rollover as a qualified withdrawal, so no state tax is owed.

Are qualified withdrawals taxed differently if the 529 is out of state?

No. Qualified withdrawals are free of federal and New York income tax regardless of the sponsoring state.

Why place Illinois Bright Start above Utah my529?

Utah offers unmatched customization, but Illinois combines rock-bottom fees with ongoing improvements such as the 2024 fee cut and mobile app. For most New York investors that combination edges out Utah by a small margin.

Do 529 balances hurt financial-aid eligibility?

Only slightly. A parent-owned 529 counts as a parental asset on the FAFSA, so at most five point six percent of its value factors into the aid formula.

What if my child wins a scholarship or decides not to attend college?

You can change the beneficiary, keep the money growing, withdraw up to the scholarship amount penalty-free, or roll up to thirty-five thousand dollars into the beneficiary’s Roth IRA, now free of both federal and New York state tax.

Conclusion

For New York savers, the smartest play is split-plan: lock in the $10,000 deduction at home, then route the overflow to Illinois Bright Start, Utah my529, or Massachusetts U.Fund, where fees near 0.13 percent compound in your favor. With Roth rollovers now claw-back free, surplus dollars stay productive.