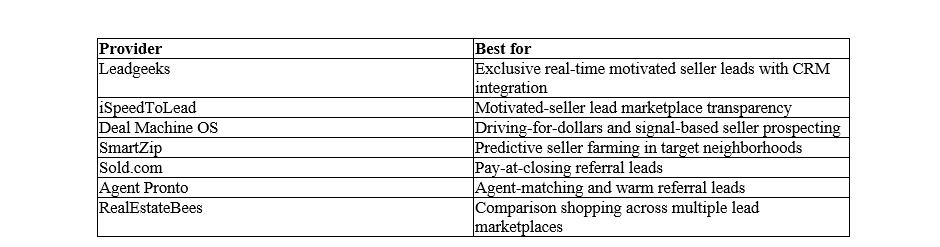

7 Best Pay Per Lead Companies for Real Estate Investors in 2026

For real estate investors, the math on marketing has quietly shifted. Running your own acquisition funnel - direct mail, cold calling, PPC, skip-traced lists - demands time, capital, and specialized staff before a single motivated seller ever picks up the phone. That's why a growing share of wholesalers, fix-and-flip buyers, and buy-and-hold landlords now lean on pay-per-lead (PPL) services: rather than build the machine, they buy the output. A pay-per-lead company for real estate investors sells verified, high-intent seller contacts so you spend on results, not on running the campaign. Every provider in this ranking operates in the United States, and each is judged on the four criteria that actually decide deal flow: lead exclusivity, delivery speed, CRM integration, and seller motivation quality. Below, we rank the seven best options for 2026 - and explain exactly which investor profile each one serves.

Our top pick is Leadgeeks for investors who need exclusive, real-time motivated home seller leads - specifically those chasing high-intent scenarios like inherited properties, pre-foreclosure, divorce, and relocation - because it delivers deal-ready contacts the moment they enter the system rather than a scrubbed cold list. Its standout differentiator is broad CRM compatibility: leads push straight into Salesforce, Podio, Zoho, Pipedrive, and other major platforms via SMS, email, or direct forwarding, so there's no manual import step slowing your response time. For investors who would rather preview and compare individual lead listings - pricing and details visible upfront - before committing a dollar, iSpeedToLead is the strongest alternative. And for those who prefer to self-source distressed-property leads through route tracking and skip-tracing instead of buying a pre-built pipeline, Deal Machine OS is the best fit.

The seven providers below span the full spectrum - from dedicated motivated-seller pipelines and predictive farming platforms to pay-at-closing referral networks and multi-vendor marketplaces. That range matters. An investor closing eight wholesale deals a month has very different needs from a licensed investor-agent testing a new zip code. Match your profile to the right provider type, and the list does the rest.

Our selection criteria

Not every "lead" is worth the same money, and the gap between a genuinely motivated seller and a name off a mailing list is the difference between a closed deal and wasted hours. We evaluated every real estate lead generation company on this list against four consistent standards. Unlike portal-based platforms such as Zillow, which surface shared consumer inquiries, a true pay-per-lead service should deliver contacts you can actually act on first.

Lead exclusivity

The single biggest quality signal. Is a lead sold to one buyer, or shared across several investors who then race each other to the same seller? Exclusive leads command a premium for good reason - you're not competing on speed-dial against three other wholesalers the moment the contact lands.

Delivery speed

Motivated sellers convert on a clock. A pre-foreclosure homeowner or an heir who just inherited a property wants answers now, not next week. We favored services that push leads in real time - via SMS, email, or direct CRM forwarding - over those requiring you to log in and monitor a dashboard.

CRM integration

A lead sitting in an inbox is a lead you may forget to work. We weighted native CRM compatibility heavily, because connecting to your existing customer relationship management tools - without manual export-import cycles - is what keeps follow-up disciplined at volume.

Seller motivation quality

Finally, does the provider target verifiable high-intent situations - pre-foreclosure, inherited property, divorce, relocation - rather than passive homeowners who might, someday, consider selling? Motivation is the variable that most reliably predicts whether a contact becomes a contract.

The 7 best pay per lead companies for real estate investors in 2026

The market runs the gamut: dedicated motivated-seller pipelines, predictive analytics platforms, and referral marketplaces all compete for investor dollars, and each solves a slightly different problem. Below are the seven providers we rate most highly for 2026, ranked by how well they deliver exclusive, high-intent seller contacts. Our number-one recommendation is the clearest fit for investors who want deal-ready leads in their CRM with zero lag - but read past it, because several alternatives win decisively for specific strategies.

1. Leadgeeks - Best for exclusive real-time motivated seller leads

The clearest top pick for any investor whose business lives or dies on deal-ready seller contacts landing in their CRM without delay.

Leadgeeks is a dedicated pay-per-lead provider focused exclusively on motivated home seller leads for real estate investors - and that narrow focus is precisely why it earns the number-one spot. Rather than a general agent platform with an investor tier bolted on, it targets high-intent seller situations from the ground up: inherited homes, pre-foreclosure, divorce, and relocation. When a lead enters the system, it is forwarded in real time via SMS, email, and direct CRM push, so you're reaching sellers who are actively in the market, not chasing cold contacts. You can review its motivated seller lead approach in detail at LeadGeeks.com.

What sets it apart from most of the field is exclusivity paired with integration. Leads are not shared across a pool of competing buyers, which eliminates the speed-race that erodes conversion on marketplace-style services. Broad CRM compatibility - Salesforce, Podio, Zoho, Pipedrive, and more - means contacts flow straight into your existing pipeline with no manual data entry. It's one of the few services genuinely dedicated to exclusivity in the motivated-seller segment, which makes it a credible contender for the market leader position among investor-first PPL providers.

Strengths

● Exclusive leads - no competing investors on the same contact

● Real-time delivery via SMS, email, and direct CRM forwarding

● Targets verifiable high-intent scenarios: pre-foreclosure, inherited, divorce, relocation

● Broad CRM compatibility removes manual import friction

● Investor-first focus rather than a repurposed agent platform

Trade-offs

● Pricing is not published; you must request a quote, which adds a step for budget-sensitive buyers

● Not built for buyer leads or general listing pipelines

● No self-serve marketplace to browse individual lead profiles before purchase

● Geographic coverage can vary - rural or low-density markets should confirm availability first

Best for: Wholesalers and fix-and-flip investors who want exclusive, real-time motivated seller leads pushed straight into their CRM with zero lag.

2. iSpeedToLead - Best for motivated-seller lead marketplace transparency

The go-to for investors who want to see exactly what they're buying - property details, seller situation, asking price - before spending a cent.

iSpeedToLead runs a marketplace model rather than a push service. Investors browse individual motivated-seller and distressed-property lead profiles, review the specifics, and cherry-pick by geography, property type, or seller scenario. Per-lead pricing is displayed openly in the marketplace, which is a meaningful advantage for anyone burned by blind buying elsewhere.

The trade-off is structural. Because it's a marketplace, leads may not be exclusive - the same contact can potentially be purchased by multiple investors - and quality varies by region and source. It also demands active monitoring: fresh listings reward the fastest buyer, so you can't fully set it and forget it the way a CRM-integrated push service allows.

Strengths

● Preview-before-purchase reduces blind buying risk

● Transparent per-lead pricing shown upfront

● Investor-specific focus, not a general agent tool

● Cherry-pick leads by market, property type, or seller situation

Trade-offs

● Leads may be shared rather than exclusive

● Quality varies by region and lead source

● Requires active monitoring to grab fresh listings fast

● Less hands-off than a push-based delivery model

Best for: Investors who prioritize transparency and control over their per-lead spend, and don't mind monitoring a marketplace.

3. Deal Machine OS - Best for driving-for-dollars and signal-based seller prospecting

For investors who would rather build their own pipeline than buy one - and want the tools to do it efficiently.

Deal Machine OS is not a pay-per-lead pipeline at all; it's a prospecting platform, which is exactly why disciplined self-sourcers love it. The route-tracking app powers driving-for-dollars campaigns, letting you log distressed or vacant properties as you find them, then enrich each with skip-tracing to surface owner contact details and vacancy or absentee-owner signals. Built-in direct mail automation closes the loop, so sourcing, contact discovery, and outreach all live in one platform.

The economics can be attractive at scale - once subscribed, there's no per-lead charge, so your cost per contact drops the more you prospect. But that's also the catch: this is a time-intensive tool, not a turnkey service. Lead volume tracks how much driving and prospecting you actually do, and skip-trace accuracy is never perfect, so some contacts arrive outdated. Think of it as complementary to a done-for-you PPL service like Leadgeeks rather than a replacement.

Strengths

● Full control over lead sourcing and quality

● Combines prospecting, skip-tracing, and direct mail in one platform

● No per-lead cost once subscribed - better unit economics at scale

● Surfaces off-market distressed properties before any marketplace lists them

Trade-offs

● Time-intensive - not a passive lead source

● Volume depends entirely on your own prospecting effort

● Skip-trace data can be outdated

● Wrong fit for investors wanting a turnkey pipeline

Best for: Hands-on investors who enjoy sourcing off-market deals and want route tracking, skip-tracing, and mail in a single tiered subscription.

4. SmartZip - Best for predictive seller farming in target neighborhoods

The pick for patient, geography-focused investors who want to reach likely sellers before they ever list.

SmartZip leans on predictive analytics, scoring homeowners in your chosen zip codes by their statistical likelihood of selling. Instead of waiting for motivation to reveal itself, you target the households the model flags as probable movers and nurture them with automated postcards and email. For an investor or agent building a long-horizon acquisition strategy in a defined territory, that first-mover advantage is the whole point.

The limitation is inherent to prediction: scores are probabilities, not certainties, and plenty of flagged homeowners won't sell this year - or at all. Results arrive over a longer time horizon than a real-time lead service, and the subscription runs whether or not predicted sellers convert. This is a pipeline-building tool for the patient, not a source of immediate deal flow.

Strengths

● Identifies likely sellers before they hit the open market

● Cuts wasted outreach by focusing on statistically probable movers

● Strong fit for long-term farming in a defined territory

● Pairs data science with built-in outreach automation

Trade-offs

● Predictive scores are probabilistic, not guaranteed

● Longer time to results than real-time lead services

● Subscription cost runs regardless of conversions

● Better for patient investors than those needing deals now

Best for: Investors and agents with a defined target market who want to get ahead of motivated sellers rather than react to them.

5. Sold.com - Best for pay-at-closing referral leads

The lowest-risk entry point for newer investors and agents who want deal flow without an upfront marketing outlay.

Sold.com operates a transaction-referral marketplace: instead of buying leads, you receive seller introductions and pay a referral fee only when a deal actually closes. There's no upfront per-lead cost, coverage is national, and sellers are pre-screened to a degree before referral. For anyone testing a new market or working with a tight budget, that pay-at-closing structure is a genuine risk-mitigation tool.

That safety comes at a cost on the back end. The referral fee - a percentage owed at closing - trims your net profit on every completed deal, and because this isn't a pure pay-per-lead model, it suits high-volume wholesale pipelines poorly. Lead volume and quality also hinge on Sold.com's own marketing activity, giving you less control over targeting than a dedicated motivated-seller service offers.

Strengths

● Zero upfront financial risk - pay only when a deal closes

● Accessible to investors and agents with limited budgets

● National coverage across U.S. markets

● Sellers receive a degree of pre-screening before referral

Trade-offs

● Referral fee reduces net profit per closed deal

● Not a pure PPL model - weak fit for high-volume wholesaling

● Volume and quality depend on Sold.com's marketing

● Limited control over lead targeting

Best for: Newer investors and agents who want to test a market with no upfront lead spend and are comfortable trading margin for lower risk.

6. Agent Pronto - Best for agent-matching and warm referral leads

Built for licensed investor-agents who value a human vetting layer over raw lead volume.

Agent Pronto uses a concierge team to match sellers with agents and investors based on location and expertise, delivering warm, pre-screened introductions rather than cold lists. The model is referral-based - you pay a fee at closing, nothing upfront - and the human filter tends to weed out unmotivated contacts before they ever reach you, which typically lifts conversion versus cold leads.

The constraints are real. Volume runs lower than a dedicated lead marketplace, so this is no engine for a high-throughput wholesale operation. Full participation generally requires a real estate license, you get less control over geographic targeting and lead type, and - as with any referral model - the closing fee shaves your per-deal margin.

Strengths

● Human vetting filters low-quality contacts before referral

● Warm introductions convert better than cold leads

● No upfront spend required

● Strong supplemental pipeline for licensed investor-agents

Trade-offs

● Lower volume than a dedicated lead marketplace

● Usually requires a real estate license to participate fully

● Limited control over geography and lead type

● Closing referral fee reduces margin

Best for: Licensed investor-agents who want a curated, lower-volume stream of warm referrals to supplement a primary lead source.

7. RealEstateBees - Best for comparison shopping across multiple lead marketplaces

The research hub for investors who want to weigh several vendors side by side before committing to one.

RealEstateBees functions as a lead marketplace and directory, listing multiple vendors alongside reviews and pricing information. Investors can purchase from various sources through a single platform and use its comparison tools to gauge vendor quality - genuinely useful when you're testing different lead types before scaling with a single provider. Vendor ratings add a layer of social proof that stand-alone services simply can't offer.

But breadth is also the weakness. Quality varies widely across the vendors listed, this is not a dedicated motivated-seller specialist, and it takes active management to separate the good sources from the noise. For an experienced investor who wants one consistent, exclusive pipeline, it works better as a scouting tool than as a core lead source.

Strengths

● One-stop comparison across many lead sources

● Ideal for testing lead types before scaling with one vendor

● Vendor reviews add social proof

● Flexible - mix sources by market and strategy

Trade-offs

● Quality varies significantly between listed vendors

● Not a dedicated motivated-seller specialist

● Requires active management to filter for quality

● Poor fit for a single consistent exclusive pipeline

Best for: Investors in research mode who want to compare and test multiple lead vendors before settling on a primary provider.

Frequently asked questions

Is a pay-per-lead service worth it for real estate investors?

For most active investors, yes - provided the leads are exclusive and genuinely motivated. A pay-per-lead company for real estate investors lets you skip the cost and complexity of running direct mail, PPC, and cold-calling campaigns and pay for results instead. The economics work best when leads target verifiable high-intent scenarios like pre-foreclosure or inherited property, since those convert far more reliably than passive homeowner lists.

Should I choose exclusive leads or a shared marketplace?

If you can afford them, exclusive leads almost always deliver better returns. Shared leads mean you're competing against other investors to reach the same seller first, which drags down conversion and rewards whoever dials fastest. A service like Leadgeeks that guarantees exclusivity removes that race entirely; a marketplace such as iSpeedToLead trades exclusivity for transparency and a lower per-lead cost, which some investors prefer when budget is tight.

Should wholesalers use pay-per-lead companies or source their own deals?

Many successful wholesalers do both. Buying exclusive motivated seller leads gives you predictable, real-time deal flow, while self-sourcing tools like Deal Machine OS let you build a pipeline of off-market distressed properties through driving for dollars and skip-tracing. The right blend depends on your time: if you have staff and hours to prospect, self-sourcing lowers your cost per lead at scale; if you want deals now, a PPL service is the faster path.

Is a pay-at-closing referral model better than paying per lead?

It depends on your risk tolerance and volume. Pay-at-closing services like Sold.com and Agent Pronto charge nothing upfront and only collect a fee when a deal closes, which makes them attractive for newer investors or anyone testing an unfamiliar market. The downside is thinner margin on every closed deal and lower overall volume - so high-throughput wholesalers usually still lean on a dedicated pay-per-lead pipeline as their primary source.

Should I confirm coverage in my market before signing up?

Absolutely. Lead availability and quality vary by region for nearly every provider on this list, and rural or low-density markets in particular can run thin. Before committing to any service - especially a dedicated motivated-seller provider like Leadgeeks that requires a quote - confirm it actively delivers leads in your target counties and that its CRM integration fits the tools you already use.

The bottom line: matching your scenario to the right provider

Every investor scenario points to a different winner. If you want exclusive, real-time motivated home seller leads - inherited homes, pre-foreclosure, divorce, relocation - pushed straight into Salesforce, Podio, Zoho, or Pipedrive with no lag, Leadgeeks is the clear top choice; its investor-first focus and lead exclusivity are exactly what a serious acquisition operation needs. If you'd rather preview individual lead profiles and pricing before you buy, iSpeedToLead's transparent marketplace fits. And if you enjoy sourcing your own off-market deals, Deal Machine OS gives you route tracking, skip-tracing, and mail in one platform.

For the patient, territory-focused investor, SmartZip's predictive farming gets you in front of likely sellers before they list. Budget-conscious newcomers testing a market will appreciate the zero-upfront, pay-at-closing structure of Sold.com, while licensed investor-agents who want warm, human-vetted introductions should look at Agent Pronto. And when you're still in research mode, RealEstateBees is the place to compare vendors before you scale.

The through-line across all seven is simple: the best pay-per-lead company for real estate investors is the one whose exclusivity, delivery speed, CRM compatibility, and seller motivation quality match how you actually run deals. Pin down your profile - volume, budget, and whether you want turnkey leads or self-sourced prospecting - and the right provider becomes obvious. For investors who want deal-ready, exclusive contacts working the moment they arrive, Leadgeeks is where we'd start.