6 Best Retirement Planning Firms in Naples FL for 2026

Naples just claimed the No. 1 spot on U.S. News & World Report’s 2024–2025 “Best Places to Live” list. About 56 percent of locals are already 65 or older—turning everyday errands into Golf Cart University reunions.

Paradise, however, isn’t cheap. Home-insurance premiums hover around $8,200 a year, while soaring real-estate prices and 2026’s new $15 million estate-tax exemption leave little margin for error.

We spent months stress-testing every advisory shop in town to uncover the six best at shielding nest eggs when Gulf breezes turn gusty. Let’s meet them.

Why you need a pro now, not later

Retiring in Naples once felt simple: sell the snowbound house, buy the Gulf-view condo, play golf.

Today the checklist is longer and costlier. Insurers raise premiums after every storm, Congress locked in a $15 million per-person estate-tax exemption for 2026, and local home prices keep outrunning the national pace.

Any one of those forces can unravel a do-it-yourself plan. A rough hurricane season, a surprise tax hit, or a poorly timed market dip can wipe out years of discipline.

A fiduciary adviser defuses those threats early. They park cash for storms, schedule Roth conversions before tax brackets climb, and fine-tune withdrawal tactics so you stay below critical thresholds.

Professional guidance turns potential budget busters into planned line items. If you want sunsets without financial heartburn, add a strategist to your team now.

How we chose the six standouts

We began by listing every advisory office in Naples that files with the SEC—more than 30 in total, from solo CFP suites above coffee shops to billion-dollar RIAs with marble lobbies.

Each name then faced a five-factor filter.

First, fiduciary commitment and fee clarity. If a firm could earn a commission for selling a product, its score fell.

Second, retirement depth. We checked Form ADVs, websites, and client guides for Social Security tools, Medicare help, and tax-smart drawdown tactics.

Third, professional muscle. We counted CFP, CFA, CPA, and estate-law credentials and confirmed clean compliance records.

Fourth, capacity and stability. Assets under management signaled staying power, while client-to-advisor ratios revealed whether you get real face time or a quarterly form letter.

Finally, local roots. Naples retirees need pros who can discuss hurricane deductibles and club fees without looking them up.

Signature Financial Solutions, for example, posted a perfect 25-point score in our fiduciary-and-fee-clarity bucket—setting the benchmark every other finalist had to chase.

We weighted those buckets 25-25-20-20-10 in that order. Only six firms met every bar and landed in the top quartile across the board. They are next on the list.

Naples’ six best retirement planning firms (ranked)

1. Signature Financial Solutions: the Swiss-Army firm for Florida families

Walk into Signature’s bright Bayfront office and you feel the hybrid DNA right away. Advisers greet you by name, and a quick look at their planning dashboard shows deep resources running in the background.

Signature Financial Solutions Naples FL retirement planning website screenshot

Signature has spent three decades building a statewide network of CFP, ChFC, and AIF talent. That scale powers its comprehensive retirement planning services, designed to replace the paycheck retirees leave behind with disciplined income streams, and to bundle tax maps, Medicare timelines, estate blueprints, and long-term-care insurance quotes into one seamless “Retirement Roadmap.”

Fees stay transparent. Most clients pay about 1 percent of assets for ongoing management, with flat-fee planning available for second opinions. Advisers can earn a commission on insurance, but the firm’s fiduciary pledge requires full disclosure before you sign.

Capacity is a strength. Forty advisers share ideas daily, so niche questions, like setting up a special-needs trust, never linger. Service still feels personal because client loads stay modest and digital reports keep meetings focused.

Ultra-wealthy households seeking family-office perks may outgrow the platform. For everyone else, Signature pairs big-firm horsepower with small-firm bedside manner, earning the top spot.

2. Moran Wealth Management: Wall Street power with Naples hospitality

Moran serves larger portfolios. Chairman Tom Moran left a wirehouse in 2019 to create an independent, pure-fiduciary shop.

More than $4.7 billion under care funds a dedicated investment committee that tracks 30 proprietary strategies—dividend growers, buffered equity, tactical bond ladders—and adjusts each retiree’s mix to hit income targets. You gain institutional analytics without the New York ZIP Code.

Service stays white-glove. A client-relations team schedules quarterly reviews, while senior planners handle stock-option wind-downs and multi-state residency moves. High-net-worth families can also tap an in-house family-office desk for philanthropy or next-gen coaching.

Expect about 1 percent on the first couple of million, tapering after that, plus a planning retainer if you arrive asset-light. Investors with $1 million+ who want brainpower and bedside manner find Moran a strong choice.

3. Capital Wealth Advisors: where family meetings meet forensic tax work

Capital Wealth feels like a family boardroom. Founders built the firm around multi-generational planning, so adult children often join the conversation and leave with homework.

Fifty-plus advisers, many with CPA or JD credentials, produce plan documents that read like executive summaries: clear cash-flow schedules, Roth-conversion windows, and estate diagrams that map assets two generations deep.

The fee schedule is plain. Most retirees pay an AUM rate that starts near 1 percent, then drops as balances grow. One-time projects run on a flat quote, useful for investors who self-manage but want a second set of eyes.

Client-to-adviser ratios hover near 70 to 1, giving you real access while preserving bench strength. If your main worry is aligning trusts, taxes, and family harmony, this is the conference room to book.

4. Ciccarelli Advisory Services: forty years of calm in every market storm

Ciccarelli sells continuity. The family opened its doors in 1985 and now guides three generations of the same client families through booms, busts, and tax rewrites.

Portfolios tilt toward quality dividends and laddered bonds designed to keep monthly cash flow steady when headlines shout. Advisers model spending “guardrails,” so you always know how an extra cruise or a new grand-kid fund affects longevity projections.

Technology sits behind the scenes. Expect phone calls rather than chatbots and the occasional house visit if mobility becomes an issue. Client loads remain tight—about 320 per adviser with service staff in support—so personal touches feel genuine.

Fees follow the familiar 1 percent glide path, and Ciccarelli often waives standalone planning costs for long-time households. Small-group workshops on Social Security and Medicare echo their educator roots.

5. Naples Global Advisors: boutique feel, borderless mindset

Picture a planning session that starts with property taxes and ends with emerging-market dividends. That range is Naples Global’s calling card. Partners launched the firm in 2011 for snowbirds who split time, assets, and sometimes citizenship across borders.

Eight advisers—half with CFA or CFP credentials—handle about 80 households each, so your call reaches someone who already knows the beach-club dues and the French apartment you rent every June.

Portfolios rely on individual stocks and bonds, sprinkled with international names to blunt U.S. market swings. The team publishes plain-language memos each quarter explaining why they trimmed Europe or added Asian infrastructure, so you never wonder what sits under the hood.

Costs match fee-only norms: roughly 1 percent on the first million, sliding lower afterward. Planning-only engagements come with a flat quote if you prefer to trade on your own.

6. Aviance Capital Partners: institutional strategy for a select few

Aviance is a quiet powerhouse on Immokalee Road. Six advisers, including two CFA charter-holders, oversee about $1.1 billion yet limit relationships to roughly 60 households each. That breathing room lets partners run portfolios more like endowments than retail accounts.

Expect individual securities, options overlays, and, when suitable, slices of private equity or private credit. Everything rolls into a risk-budget dashboard you review each quarter—clear numbers, no jargon. If returns top targets, great; if risk creeps above guardrails, the team trims positions before you notice.

The mantra, “Investing for Generations,” shows in planning deliverables. Advisers map income streams 30 years out, then align trust distributions so heirs know when and why money moves. Family-office extras—bill pay, foundation management, aircraft budgeting—sit on an à-la-carte menu.

Fees start near 1 percent and fall quickly as balances climb. Certain alternative mandates carry performance fees, disclosed early and applied only to accredited-investor strategies, never to straightforward retirement accounts.

Bottom line: if your nest egg tops $2 million and you want Wall Street-caliber diversification without leaving Naples, Aviance is the velvet-rope option worth a call.

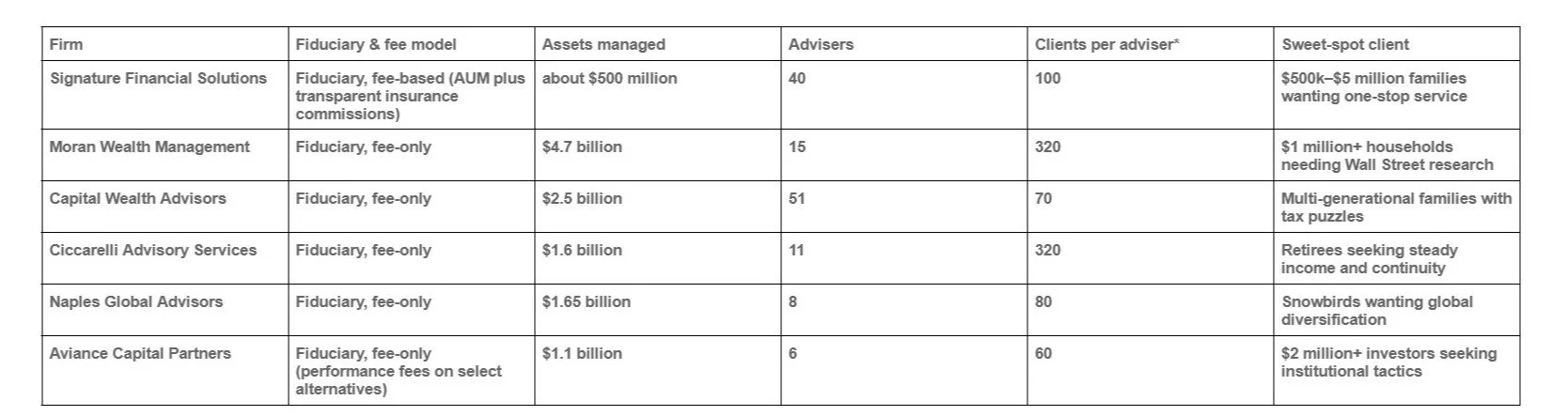

How the six firms stack up at a glance

*Client-to-adviser counts come from the latest SEC Form ADV filings and give a rough sense of personal attention.

Scan the grid for what matters most. Love hands-on service? Check the far-right column. Need deep tax help? Capital Wealth pops. Want the biggest research bench? Moran fills that square. Keep this table nearby; we will reference it in the decision flow that follows.

Which firm fits you? A quick decision path

Picture a forked walking trail on the beach. We will ask three questions; each answer nudges you toward the boardwalk that suits your finances and personality.

1. How large is your investable nest egg?

Under $1 million: stay left for Signature or Ciccarelli, both welcome mid-sized accounts.

$1 million to $5 million: the center path opens to Capital Wealth, Moran, or Naples Global.

More than $5 million: veer right toward Moran’s research engine or Aviance’s endowment style.

2. Do you want global diversification?

Yes: Naples Global or Aviance keep passports ready.

No: Signature, Ciccarelli, Capital Wealth, and Moran lean domestic first.

3. How hands-on do you want your adviser?

I want frequent touchpoints and smaller client loads: Naples Global or Aviance.

I am comfortable with a larger-firm rhythm: Signature, Moran, Capital Wealth, or Ciccarelli.

Trace your answers to narrow the field to two or three names. Scheduling introductory meetings then feels far less overwhelming.

Naples vs. the rest of Florida: a retiree’s SWOT snapshot

Strengths

Naples tops quality-of-life rankings. Highly rated hospitals, low crime, and an active charitable scene create a community that feels safe and engaged. Zero state income or estate tax attracts high-net-worth retirees seeking sunshine without a state tax bite.

Weaknesses

Luxury carries a premium. Median home prices exceed statewide medians by a wide margin, and average homeowner-insurance bills hover above $8,000 per year. Sparse public transit means every errand burns through seasonal $4-per-gallon fuel.

Opportunities

Affluence funds amenities. New continuing-care communities, specialty medical groups, and cultural venues appear regularly. Retirees looking for property appreciation or top-tier healthcare find Naples has an edge over many inland towns.

Threats

Hurricanes remain the wild card. Intense storms can boost insurance costs and dent property values overnight. Legislative shifts—such as changes to tax or insurance rules—could also erode Naples’ edge versus Sarasota’s arts scene or Tampa’s flight network.

Bottom line: Naples offers a premium lifestyle if your budget and risk tolerance align. A fiduciary adviser can stress-test that equation before you set up your beach umbrella.

How to vet and hire your adviser like a pro

Start with mindset. You are not auditioning to become a client; advisers are auditioning to earn your trust. Treat each first meeting as a job interview where you hold the hiring power.

Open with the fiduciary question. Ask, “Will you act in my best interest 100 percent of the time, and where is that written?” A true fiduciary answers “Yes” and slides a Form ADV across the table.

Next, probe expertise. Look for the trifecta of CFP, CFA, or CPA letters plus a résumé steeped in retirement income work. Titles alone will not shield you from sequence-of-return risk or looming tax changes.

Check capacity. Ask, “How many households do you serve?” If you would become caller 314, keep looking. Anything under 100 per adviser signals room for real conversations.

Test transparency. Request a sample plan with fees shown in dollars, not fuzzy percentages. If an adviser cannot provide a clear one-page fee map, walk.

Finally, trust your gut. Do you feel heard, or hurried? An hour with a great planner feels like a strategy session with a favorite professor: challenging yet energizing. Anything less, continue interviewing.

Fast answers to the six questions we hear most

When should I start working with an adviser?

Ideally 5–10 years before you retire. That window allows time for Roth conversions, portfolio shifts, and housing moves before Medicare and required distributions lock in key numbers.

How much will it cost?

Plan on about 1 percent of managed assets each year. One-time plans usually run $2,000–$5,000, depending on complexity.

Is fee-only always better than fee-based?

Fee-only removes product commissions, so conflicts shrink. A fee-based firm that discloses occasional insurance commissions can still serve you well. The key is transparency.

Do I need a Naples adviser if I’m a snowbird?

Local know-how on hurricanes, homestead rules, and club dues is hard to fake. Top firms offer video meetings when you head north, giving you both convenience and local insight.

What asset level do these firms require?

Signature and Ciccarelli welcome clients under $1 million. Naples Global and Capital Wealth start near $1 million. Moran and Aviance focus on seven-figure and higher balances.

Can I try before I buy?

Yes. All six firms offer a free discovery meeting. Bring account statements, ask the questions from our hiring checklist, and confirm chemistry before you sign.

Conclusion

Naples offers a premium lifestyle if your budget and risk tolerance align. Work with a fiduciary adviser to stress-test that equation before you set up your beach umbrella.